Macroeconomic Performance

Macroeconomic Performance

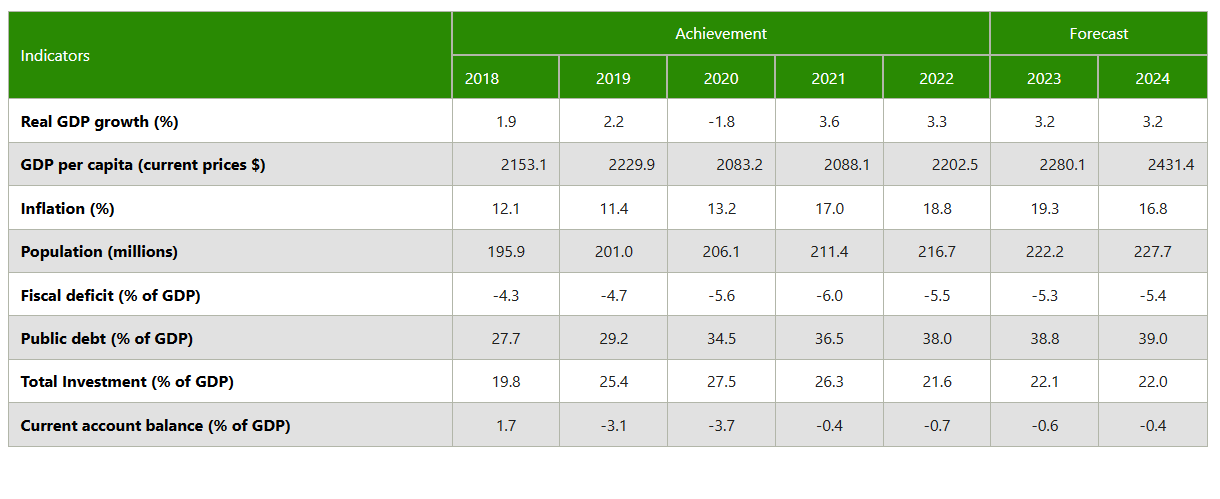

Table 1: Overview of some macroeconomic indicators

Nigeria recorded an average growth rate of 1.8 per cent over the last five years. Nigeria’s economy slowed to a growth of 3.3 per cent in 2022, down from 3.6 per cent in 2021, owing to a decline in the industry sector’s value addition (due mainly to a 19.2% decline in upstream oil and gas production) and the slow growth in agriculture (1.9%). The services sector grew by 4.5 per cent to make up for the decline and slow growth in industry and agriculture, respectively. Average inflation in the year stood at 18.8 per cent, up from 17.0 per cent in 2021, in line with the global price elevation. Fiscal balance improved to -5.5 per cent of GDP, from -6.0 per cent of GDP in 2021, with public debt and current account balance worsening to 38.0 per cent of GDP and -0.7 per cent of GDP, respectively.

Nigeria recorded an average growth rate of 1.8 per cent over the last five years. Nigeria’s economy slowed to a growth of 3.3 per cent in 2022, down from 3.6 per cent in 2021, owing to a decline in the industry sector’s value addition (due mainly to a 19.2% decline in upstream oil and gas production) and the slow growth in agriculture (1.9%). The services sector grew by 4.5 per cent to make up for the decline and slow growth in industry and agriculture, respectively. Average inflation in the year stood at 18.8 per cent, up from 17.0 per cent in 2021, in line with the global price elevation. Fiscal balance improved to -5.5 per cent of GDP, from -6.0 per cent of GDP in 2021, with public debt and current account balance worsening to 38.0 per cent of GDP and -0.7 per cent of GDP, respectively.

Outlook

Nigeria’s economy is projected to experience slow growth in 2023 due to declining upstream oil and gas production, liquidity challenges and low agricultural value addition (which has been adversely impacted by insecurity). Growth is projected at 3.2 per cent in 2023 and 2024, because of the factors enumerated above. Nigeria is looking to cut downstream petroleum subsidies, in a bid to reduce its expenditure burden. At the same time, to cushion the citizenry from the impact of this policy, there is talk of a 40 per cent increase in civil service salaries. The net effect is a projected improvement in fiscal balance, which is set to improve marginally to -5.3 per cent of GDP in 2023, before deteriorating to -5.4 per cent of GDP in 2024 but the removal of subsidies will translate into increased overall prices, thus, leading to an average inflation of 19.3 per cent in 2023, before declining to 16.8 per cent in 2024. Public debt is projected to increase to 38.8 per cent of GDP and 39.0 per cent of GDP in 2023 and 2024, respectively, while the current account balance improves to -0.6 per cent of GDP and -0.4 per cent of GDP in 2023 and 2024, respectively.

Probable Headwinds

The still high inflation will keep interest rates high. This will crowd out the private sector and repress economic growth. The removal of subsidies on downstream petroleum products and the proposed salary increases need to be handled carefully; otherwise, it could lead to civil unrest and additional fiscal costs. Nigeria must address upstream oil and gas production challenges to generate revenue to meet its expenditure and reduce the need for borrowing.